How a Bank Should Deal When a Bank Guarantee Is Invoked and the Customer Fails to Reimburse

When a Bank Guarantee (BG) issued on behalf of a customer is invoked by the beneficiary and the bank settles the claim, the bank becomes a creditor to the customer for the amount paid. If the customer fails to reimburse the bank, the bank must follow a series of operational, legal, and recovery steps as…

Read article

Non-Fund Based Facilities to Non-Constituent Borrowers: RBI Relaxation and Key Conditions

The Reserve Bank of India (RBI), through circular DBOD.Dir.BC.62/13.07.09/2002-03 dated January 24, 2003, had earlier prohibited banks from extending non-fund based facilities to non-constituent borrowers. This restriction was aimed at preventing frauds, fund diversion, and misuse of one-off transaction-based facilities without proper credit assessment. However, over time, this blanket bar created genuine challenges for borrowers…

Read article

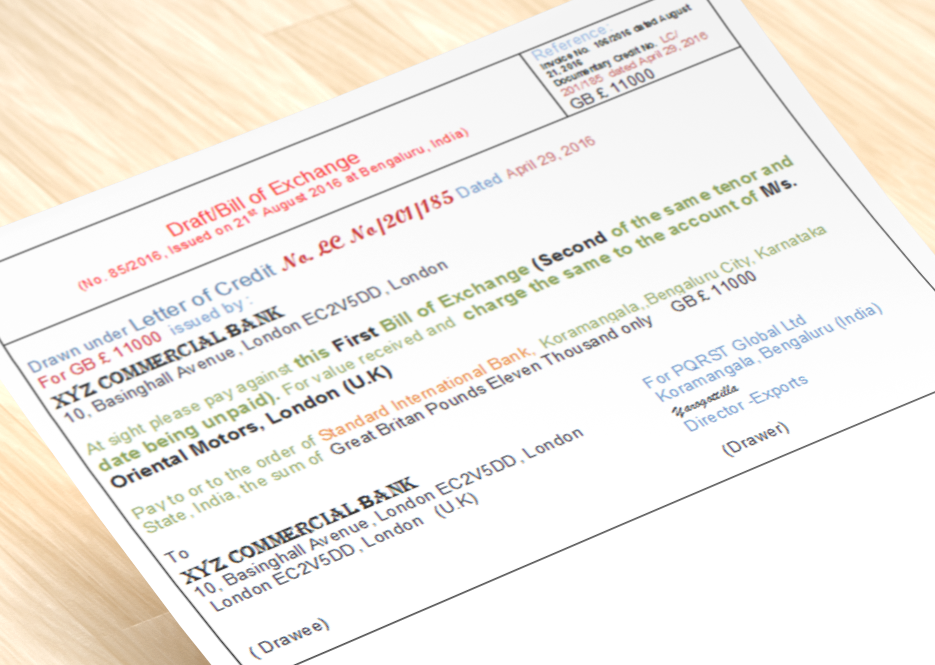

Understanding Working Capital Appraisal: Key Financial Terms Explained

The working capital requirement of industrial and trading establishments refers to the total funds invested in various current assets such as raw materials (RM), work-in-process (WIP), finished goods (FG), and outstanding receivables. Banks extend working capital facilities to borrowers based on the nature and level of current assets, after deducting the borrower’s margin contribution, within…

Read article

RBI Circular on Lending Against Silver Jewellery: Key Provisions and Compliance Framework

The Reserve Bank of India has issued standardized directions permitting loans against silver jewellery and specified silver coins, aligning silver with gold for collateralized retail lending; these directions are titled the Reserve Bank of India (Lending Against Gold and Silver Collateral) Directions, 2025 and are slated to take effect from April 1, 2026, with detailed…

Read article

Understanding Corporate Relationships: A Banker’s Guide to Subsidiaries, Sister Concerns, Associates, Joint Ventures, Conglomerates, and Groups

Introduction For bankers, understanding how different corporate entities relate to one another is more than an academic exercise—it directly impacts credit decisions, exposure limits, and regulatory compliance. Terms like subsidiary, associate company, or joint venture may sound similar, but each has a distinct legal and accounting meaning that influences how risks are consolidated and how…

Comprehensive Credit Guidelines for Pisciculture (Fish Farming) Loans: Banking SOP

Pisciculture lending involves financing fish farming activities end-to-end—from pond creation and seed stocking to feed, health care, harvesting, and marketing—with bank SOPs focusing on borrower selection, project viability, risk controls, and compliant disbursement-monitoring cycles. Banks generally offer term loans for assets (ponds, raceways, cages, aerators, hatchery equipment) and working capital/cash credit for recurring inputs (seed/fingerlings,…

Read article