The cash reserve ratio is a statutory provision regulated by RBI under Section 42(1) of the Reserve Bank of India Act 1934. Every scheduled bank (that includes public and private sector banks, foreign banks, regional rural banks, and co-operative banks) in India requires to maintaining an average balance with the Reserve Bank of India or Currency Chest Vault, which shall not be less than 3 percent of net demand and time liabilities of the bank ( At present CRR to be maintained by banks is 4 percent).

A demand deposit account (DDA) is a bank account from which deposited funds can be withdrawn at any time, without advance notice. Such deposits are considered demand liability of a bank. However, the use of methodology evolved by the RBI’s second working group on the monetary concept resulted in about 85% of savings bank deposits being classified with time deposits, the remainder were treated as demand liability. Therefore, in August 1978 Central Bank (RBI) amended the ground rule for apportioning savings deposits into demand and time deposits.

Under the new rule, the bank shall undertake the apportionment of Saving Bank Account into demand liability and time liability as per the following procedure;

- The existing system of calculation of the proportion of demand liabilities and time liabilities by Scheduled Commercial Banks in respect of their savings bank deposits on the basis of the position as at the close of business on 30th September and 31st March every year (cf. RBI circular DBOD.No.BC.142/09.16.001/97-98 dated November 19, 1997) shall continue in the new system of interest application on savings bank deposits on a daily product basis;

- The average of the minimum balances maintained (in each account) in each of the months during the half year period shall be treated by the bank as the amount representing the “time liability” portion of the savings bank deposits. When such an amount is deducted from the average of the actual balances maintained during the half year period, the difference would represent the “demand liability” portion.

- The proportions of demand and time liabilities so obtained for each half year shall be applied for arriving at demand and time liabilities components of savings bank deposits for all reporting fortnights during the next half year.

Maintaining CRR is a statutory provision, binding on scheduled banks to maintain a minimum balance at a rate decided by RBI from time to time. Banks do not get any interest on the money that is with the RBI under the CRR requirements. Besides the minimum balance of Cash Reserve Ratio to be maintained by the banks, RBI is empowered to increase it by notification up to 15 percent under the Act. RBI tries to curb inflation by increasing the CRR, wherein banks have to keep more balance with RBI, thus their lend-able resource depletes. The depleted lend-able resource of banks has a direct effect on the economy. When banks lend less, the money supply in the economy becomes scarce, naturally, demand for money goes up.

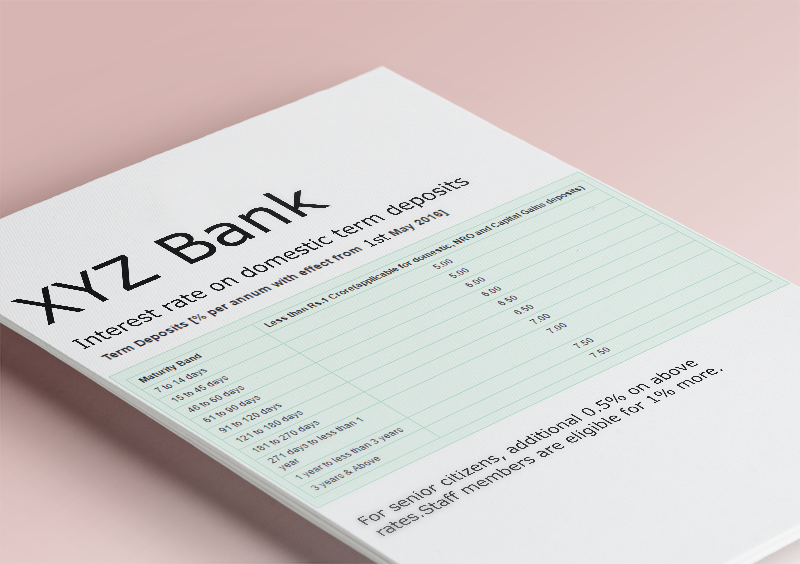

Related Post;