Both the terms credit ratings and credit scores assess creditworthiness and risk involved in lending to an entity. A credit rating agency provides an opinion relating to future debt repayments by borrowers. The rating is assigned to a security or an instrument that even assigns an issuer rating. A credit bureau (Credit information Company) provides information on past debt repayments by borrowers. Credit scores are three-digit numbers that tell lenders whether an individual is likely a responsible borrower. Credit ratings, on the other hand, are letter ratings assigned to corporations or governments. The ratings assigned to an entity or an instrument by Credit Rating Agencies (CRA) are used by investors to determine risk in investment.

When you as an individual or small business approach a lending institution for loans, that institution refers to your CIR or credit score and assesses your credibility and worth for the amount you have asked to borrow. The Credit Information bureaus are the companies that provide Credit Information Reports to your bank. Credit Information bureaus (CIB)are also known as Credit Information Companies (CIC).

Credit rating agencies (CRA) rate various entities excluding individuals as borrowers on their repayment ability using a range of metrics and factors. They determine credit ratings for corporate issuers, financial institutions, managed funds, project finance companies, structured finance companies, State Governments, and urban local bodies.

Different credit-scoring models and score ranges exist, but they typically fall into the following categories:

851-900 (Excellent): – Indicates a borrower with no payment defaults, considered low-risk.

751-850 (Good): Favourable score showing strong credit history with timely payments.

651-750 (Average): – Represents a balanced credit history with fair credit management.

501-650 (Poor): – Indicates a higher risk level, potentially due to missed payments or high credit utilisation.

300-500 (Very poor): Reflects a bad credit history with defaults and difficulties in obtaining credit.

Borrowers with lower scores may face challenges in accessing credit or may be offered higher interest rates. It’s advisable to improve a low credit score to enhance creditworthiness.

Credit information bureaus in India (CIB):

Credit Information bureaus maintain a repository of credit information of individual borrowers, offer comprehensive risk management tools, and provide lenders with portfolio reviews of borrowers that help them study a borrower’s behaviour and past or existing relationships with multiple lenders.

In India Experian, Equifax, TransUnion CIBIL, and CRIF Highmark are major authorised credit information bureaus in India. They generate a three-digit credit score and credit report after evaluating your credit history. Credit scores usually help determine the creditworthiness of individuals and are calculated based on the credit history found in the credit report. Credit scores are computed by four major credit bureaus in India including TransUnion CIBIL, Equifax, Experian, and CRIF Highmark.

It is considered that the higher the scores in the report, the chances of default is less. Generally, most of the banks accept a CIBIL TransUnion score of 750 and above level good for lending in the earlier version of scoring). Scores in the range of 300 to 600 are always considered being a risky proposal by the lender, as it indicates the past credit history of the borrower is bad. Since the chances of default are higher, in most cases, the credit proposals received from such borrowers are rejected by financial institutions without further process. However, the cut-off credit scoring for eligibility for loans may vary from bank to bank depending upon the individual bank’s loan policy.

To know how the credit score is calculated click credit score

Credit rating agencies (CRA)

Credit rating agencies (CRA) rate various entities excluding individuals as borrowers on their repayment ability using a range of metrics and factors. They determine credit ratings for corporate issuers, financial institutions, managed funds, project finance companies, structured finance companies, State Governments, and urban local bodies.

While assessing the credit rating of a sovereign the rating agencies utilize a large number of economic and other ratios. The most important variables examined include economic characteristics, Monetary Environment, Foreign Trade, Security instability, etc. A credit rating agency provides an independent evaluation of the creditworthiness of debt securities issued by governments and corporations especially their ability to meet principal and interest payments on their debts.

RBI has identified seven domestic and three international rating agencies in India that are accredited for risk weighting the banks’ claims for capital adequacy purposes. The long-term and short-term ratings issued by these credit rating agencies have been mapped to the appropriate risk weights applicable as per the Standardized approach under a Basel Framework. Based on ratings assigned by recognized Credit rating agencies banks who have such ratings may assert the risk weight of their assets. This is in line with the provisions of the revised structure of risk weight envisaged by RBI. For declaration of capital adequacy, banks may use the ratings assigned by any one of the following domestic credit agencies.

a) Credit Analysis and Research Limited(CARE);

b) CRISIL Limited;

c) India Ratings and Research Pvt. Ltd. (formerly known as FITCH India);

d) ICRA Limited;

e) Brickwork Ratings India Pvt. Limited (Brickwork);

f) SMERA ;

g) INFOMERICS Valuation and Rating Pvt Ltd. (INFOMERICS)

Reserve Bank of India also permitted banks in India to use ratings of the following international credit rating agencies for their claims for capital adequacy purposes.

a. Fitch;

b. Moody’s; and

c. Standard & Poor’s

Application of External Ratings

Banks have the option to select credit rating agencies of their choice for both risk weighting and risk management purposes. However, Banks do not have permission from RBI to “cherry-pick” the assessments provided by different credit rating agencies. If a bank decides to employ the ratings of particular credit rating agencies, for a known type of claim, it can use the ratings of those credit rating agencies. Nevertheless, some of these claims may be rated by other chosen credit rating agencies whose ratings the bank has decided not to use. However banks are not permitted to use one agency’s rating for one corporate bond, and at the same time use another agency’s rating for another exposure to the same counterparty. Anyway, it is allowed, when the respective exposures are rated by one of the selected credit rating agencies, whose ratings the bank has decided to use. External assessments for one entity within a corporate group cannot be used to risk weight other entities within the same group.

Credit ratings are usually expressed as letter grades like A1+, A1-, A2, A3, A4, etc.

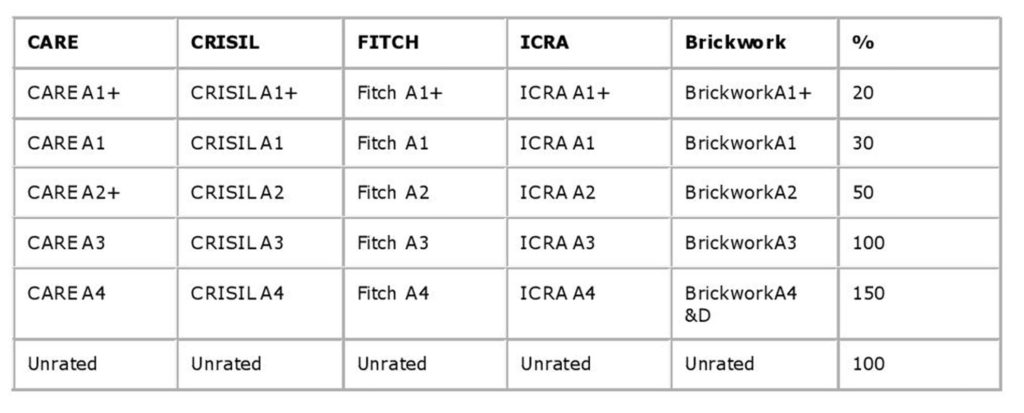

It is obligatory on the part of banks to disclose the names of the credit rating agencies that they use for the risk weighting of their assets. Risk Weight Mapping of Long-term Term Ratings of the chosen Domestic Rating Agencies is as under.

To match the global capital measures and capital standards prescribed by the Basel Committee on Banking Supervision (BCBS) framework, the Reserve Bank of India introduced a risk asset ratio system for banks (including foreign banks) in India as a capital adequacy measure. The Basel Code on capital adequacy stipulates how much capital a bank should have in place, regarding the elements of credit risk in various types of assets in the balance sheet as well as off-balance sheet business of the banks. Risk Weight Mapping of Short-Term Ratings of the Domestic Rating AgenciesWhere “+” or “-” notation is attached to the rating, the corresponding main rating category risk weight should be used. For example, A+ or A- would be considered to be in the A rating category. Where “+” or “-” notation is attached to the rating, the corresponding main rating category risk weight should be used for A2 and below, unless specified otherwise. For example, A2+ or A2- would be considered to be in the A2 rating category and assigned a 50 percent risk weight.

RelatedPosts;

Originally posted on July 22, 2014, edited and reposted on February 13, 2023

Related post:

http://86x.efb.mytemp.website/financial-analysis/what-are-the-objectives-and-benefits-of-credit-rating/