Receivables financing, also referred to as bills finance, is a facility offered by banks and financial institutions that enables businesses to convert their outstanding invoices (accounts receivable) into immediate liquidity. This form of short-term funding supports effective working capital management by bridging the gap between the delivery of goods or services and the receipt of payment.

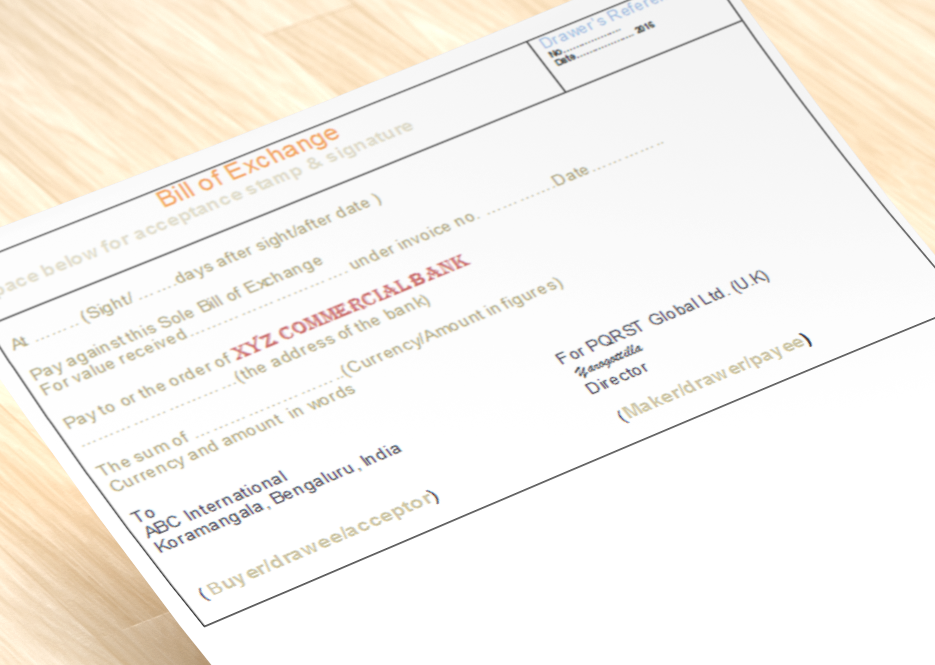

The term “bills” in this context refers to bills of exchange—negotiable instruments used in trade finance. Bills of exchange may be classified into various types such as Clean Bills, Documentary Bills, Demand Bills, Usance Bills, and Accommodation Bills. Broadly, they are grouped into two categories:

1. Documentary Bills

Documentary bills are those accompanied by documents of title to goods, which are necessary for the buyer to take possession of the shipped merchandise. Upon shipment, the seller (typically an exporter) prepares a set of documents such as the Bill of Lading, Airway Bill, Lorry Receipt (LR), Railway Receipt (RR), Dock Warrant, and Invoice. The delivery of these documents to the buyer can be structured in two ways:

- Documents against Payment (DP Bills): Documents are released only upon payment.

- Documents against Acceptance (DA Bills): Documents are released against the buyer’s acceptance of the bill of exchange.

2. Clean Bills

Clean bills are not accompanied by documents of title to goods. In international trade, “clean bills” often refer to clean bills of lading, indicating that the goods were received in good condition without any damage or defect. These are essential for ensuring smooth international trade transactions, as they assure the buyer and financiers of the quality and integrity of the goods at the point of shipment.

To know more read: “What are clean bills, documentary bills, demand bills and accommodation Bills?”

Modes of Financing Bills/Receivables by Banks

Banks extend finance against receivables using several methods, depending on the nature of the bill:

A. Purchase, Discounting, and Negotiation of Bills

Banks provide finance by purchasing, discounting, or negotiating bills presented by businesses:

- Bills Purchase: Used for financing against demand bills.

- Bills Discounting: Applicable to usance bills (bills payable after a certain period).

- Bills Negotiation: Typically used in the context of letters of credit (LC).

In all these cases, the seller (exporter) receives immediate payment from the bank, helping to maintain liquidity regardless of the underlying payment terms of the transaction.

To know more read: Difference between purchase, Discount and Negotiation of Bills

Other Forms of Receivables Finance

B. Factoring

Factoring, also known as invoice factoring or accounts receivable financing, involves the sale of receivables to a financial institution (the factor) at a discounted value. The factor then takes responsibility for collecting payments from the buyer. Services offered under factoring include:

- Collection of receivables

- Discounting of invoices

- Maintenance of sales ledgers

In domestic factoring, the seller typically receives up to 80% of the invoice value upfront, with the remaining balance paid upon final collection.

To know more read: What is Factoring?

C. Trade Receivables Discounting System (TReDS)

TReDS is an institutional mechanism regulated by the Reserve Bank of India (RBI) under the Payment and Settlement Systems (PSS) Act, 2007. It facilitates the discounting of trade receivables for Micro, Small, and Medium Enterprises (MSMEs) through multiple financiers in a competitive and transparent environment. TReDS operates in both primary and secondary market segments and aims to improve liquidity access for MSMEs.

To know more read “The complete mechanism of TReDS that helps MSME finance”

Key Benefits of Receivables Financing

- Enhanced Cash Flow: Accelerates access to funds without waiting for customer payments.

- Improved Working Capital: Supports day-to-day operations and enables business expansion.

- Financing Flexibility: Offers a range of structures suited to diverse business requirements.

- Credit-Neutral Option: Typically does not adversely affect the borrower’s credit rating.

Considerations Before Opting for Receivables Finance

- Cost Implications: Fees and interest charges are associated with the financing facility.

- Due Diligence: Lenders undertake a verification process to confirm the authenticity of receivables.

- Balance Sheet Impact: Depending on the arrangement, receivables financing may influence financial reporting and ratios.

Conclusion

Receivables financing offers a strategic tool for businesses to unlock liquidity from their trade receivables. Whether through traditional bill discounting, factoring, or platforms like TReDS, these mechanisms play a vital role in sustaining cash flow, particularly for MSMEs. The selection of an appropriate receivables finance solution depends on the company’s operational needs, customer profile, and overall financial strategy.

Disclaimer

The content provided above is intended solely for informational and explanatory purposes. It should not be considered financial advice or solicitation material. While efforts have been made to ensure accuracy, the contents are subject to change based on future amendments or judicial decisions. Readers are advised to consult with a qualified financial advisor or tax professional before making any financial or tax-related decisions.

Related Posts: