The Reserve Bank of India (RBI) has formulated a comprehensive framework to facilitate liquidity through the discounting and rediscounting of genuine trade bills. One of the key mechanisms introduced under this framework is the Bills Rediscounting Scheme (BRDS). This scheme enables banks to raise funds by issuing Usance Promissory Notes (UPNs) based on trade bills previously discounted by them.

1. Overview of the Bills Rediscounting Scheme (BRDS)

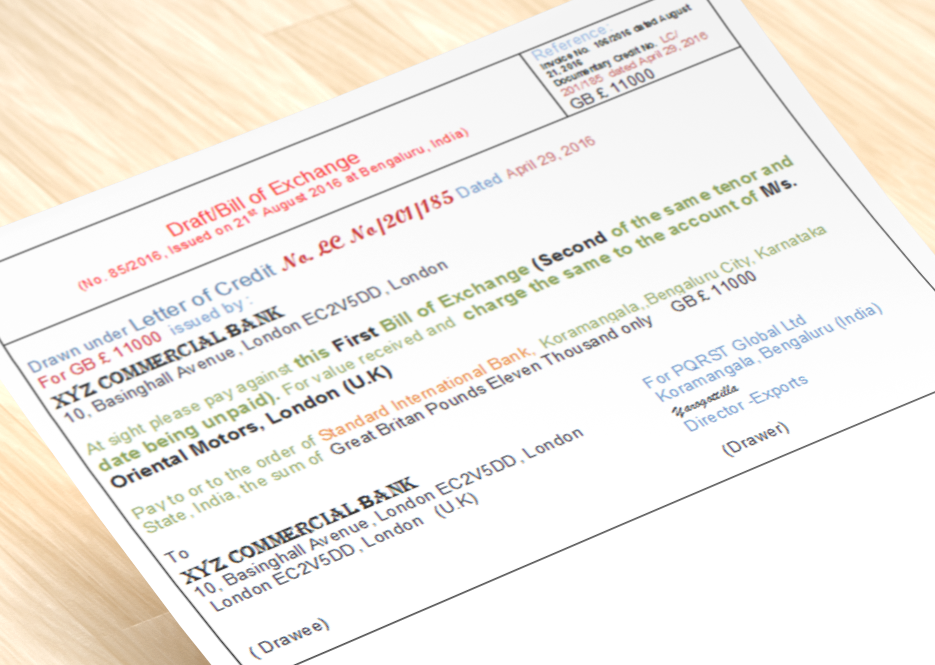

Under the BRDS, Scheduled Commercial Banks and other permitted financial entities may invest by rediscounting trade bills of eligible banks. This is done against Derivative Usance Promissory Notes (UPNs) issued by the borrowing bank. A Usance Promissory Note is a written commitment to pay a specific amount on a future date, unlike a demand promissory note which is payable on demand.

The scheme is designed to enhance liquidity in the bill market, support working capital needs of businesses, and regulate credit flows efficiently within the financial system.

2. Discounting of Bills

Definition:

Bill discounting refers to the practice where a bank purchases a bill of exchange from the holder prior to its maturity and provides immediate funds, thereby facilitating liquidity.

Eligibility:

Only genuine usance bills arising out of bona fide commercial transactions are eligible for discounting. These bills must be properly drawn and bear the requisite stamp duty.

Key Features:

- The RBI does not directly discount bills; instead, it offers refinance facilities to banks against such discounted bills.

- The UPN issued must be backed by unencumbered usance bills of at least equivalent value, which are not yet due for payment.

- Borrowing banks must issue a certificate confirming the holding of eligible bills corresponding to the value of the UPN.

- If any bills mature before the maturity of the derivative UPN, they must be replaced with fresh eligible discounted bills.

- Banks are mandated to maintain a board-approved bill discounting policy, aligned with their broader working capital finance policy.

3. Rediscounting of Bills

Definition:

Rediscounting involves the sale of already discounted bills by one bank to another financial institution before the bills’ maturity date, providing further liquidity.

Eligibility:

Only usance bills originally discounted by banks are eligible for rediscounting. Bills discounted by non-banking entities or accommodation bills (not backed by genuine trade transactions) are not eligible.

Role of the RBI:

The RBI supports the rediscounting process by offering refinance facilities to banks and by establishing guidelines and operational procedures to ensure transparency and stability in the rediscounting market.

Operational Procedure:

- Banks must verify the authenticity of the underlying trade transaction.

- Special caution is advised when dealing with bills originally discounted by Non-Banking Financial Companies (NBFCs).

- Banks are prohibited from rediscounting their own previously discounted bills.

- Finance companies and non-bank entities are not permitted to participate in rediscounting.

Simplification Measures:

The RBI has simplified rediscounting norms by:

- Allowing derivative bills for rediscounting transactions below specified thresholds (e.g., ₹10 lakh).

- Removing the restriction on minimum bill amounts.

4. Regulatory Guidelines and Considerations

Genuineness of Transactions:

Banks must ensure that all discounting and rediscounting activities are based on legitimate commercial transactions.

Due Diligence:

Appropriate due diligence must be conducted on all parties involved, including the drawer, drawee, and endorsers of the bill.

Stamp Duty:

Remission of stamp duty is available for bills of exchange drawn in favor of banks and payable within a specified period, as per government provisions.

Interest Rate Guidelines:

The RBI may prescribe interest rate norms to be followed in bill discounting and rediscounting transactions.

Monitoring and Reporting:

Banks are required to submit periodic reports and returns to the RBI for regulatory oversight of the bill market.

Market Participation:

To broaden the scope of the bill rediscounting market, the RBI has permitted participation by mutual funds and all-India financial institutions, in addition to commercial banks.

Conclusion

The RBI’s guidelines on the discounting and rediscounting of bills are aimed at fostering a robust and efficient bill market. By enabling liquidity, promoting transparent trade financing, and involving diverse financial participants, the regulatory framework seeks to strengthen the short-term credit infrastructure and maintain systemic financial integrity.

Disclaimer

The content provided above is intended solely for informational and explanatory purposes. It should not be considered financial advice or solicitation material. While efforts have been made to ensure accuracy, the contents are subject to change based on future amendments or judicial decisions. Readers are advised to consult with a qualified financial advisor or tax professional before making any financial or tax-related decisions.

Related Posts: